we'll get you approved for

6 figures of 0% interest capital

In as little as 14 days

and we'll do it all for you

By using our Funding Optimization Process to turn you from “unfundable” into an ideal client the banks

will beg to give money to.

Even if you've gotten rejected for funding before

and even if your credit isn't the best.

130+ every-day builders got approved for funding

Marcus Mcurdy

Founder of L&T Solution

marcus went from 5 months of funding rejections to getting approved for $80k in 0% interest capital in just 4 weeks

"I was honestly at my wits end. I needed cash to get through some hard times in the business. I had tried every method, tactic and strategy out there to get my hands on funding. of course nothing worked. I was ready to throw in the towel. But then I came across Citidel across an ad. Spoke to Eli and he had so much knowledge surrounding funding I decided to give them a shot. Just a month later I got approved for $110,000 in funding at 0% interest."

Rated: Excellent

Need capital to scale your business?

Please DO NOT read this

unless you absolute need to get approved for funding

Up to $150,000 of funding at 0% interest for 12-18 months.

That's essentially free money for an entire year...

Without having to resort to:

Dipping into your bank account

Maxing out your personal credit cards

Disrupting your existing cash flow

Getting taken advantage of by predatory MCA lenders

Being chained to high interest term loans

Rolling the dice on an SBA loan that won't even move the needle.

Giving away a huge chunk of the business you worked so hard to build to greedy "investors"

And what if you could get approved for that much funding even if you've gotten rejected dozens of times…

Or if your credit score starts with a 6…

Or even a 5…

"Bullsh*t"

We know, that sounds utterly ridiculous.

But in the next few paragraphs we're going to show you, step-by-step, how we used a new process called "Funding Optimization"…

To turn business owners who keep hearing "no" every time they apply for funding…

Into irresistible clients the banks practically beg to give funding to.

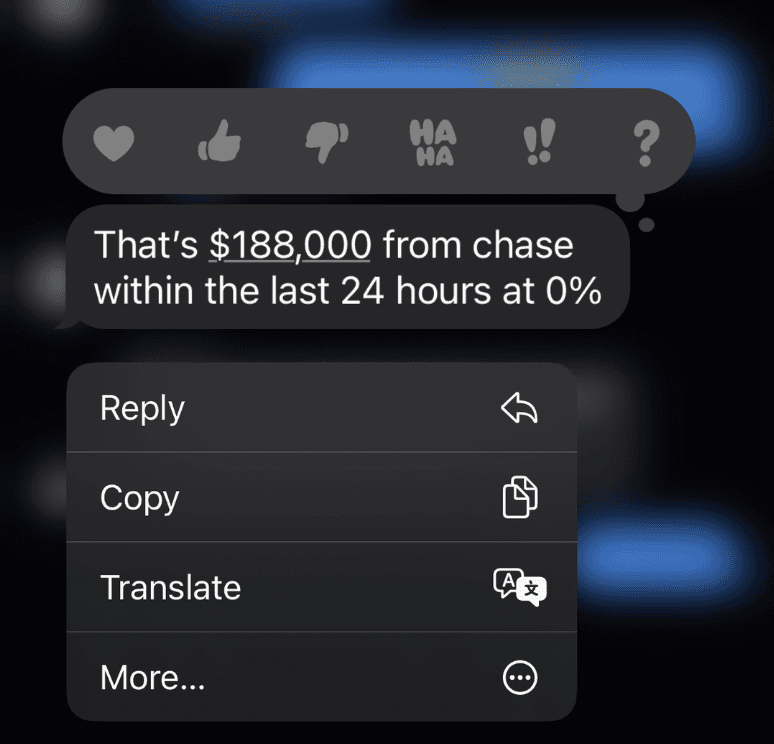

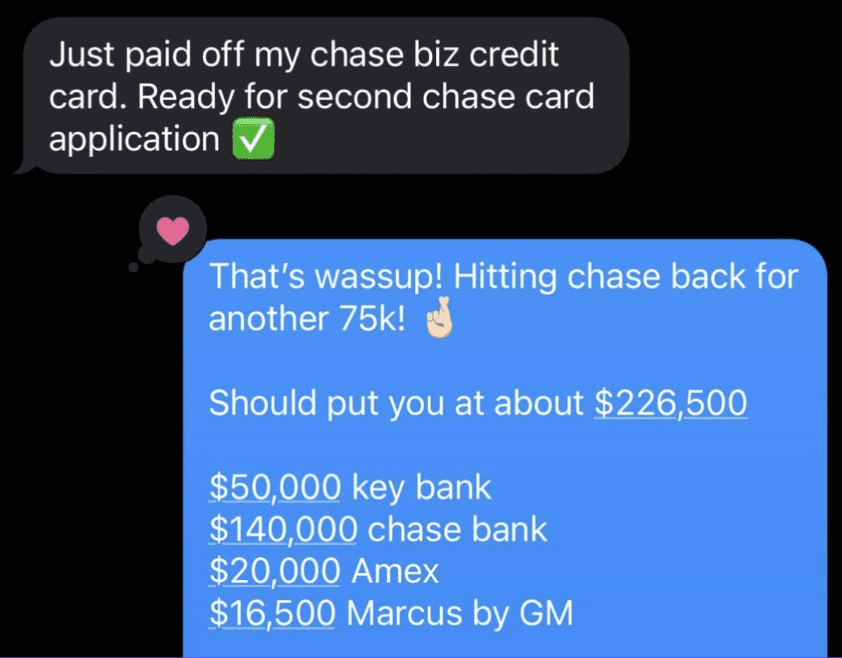

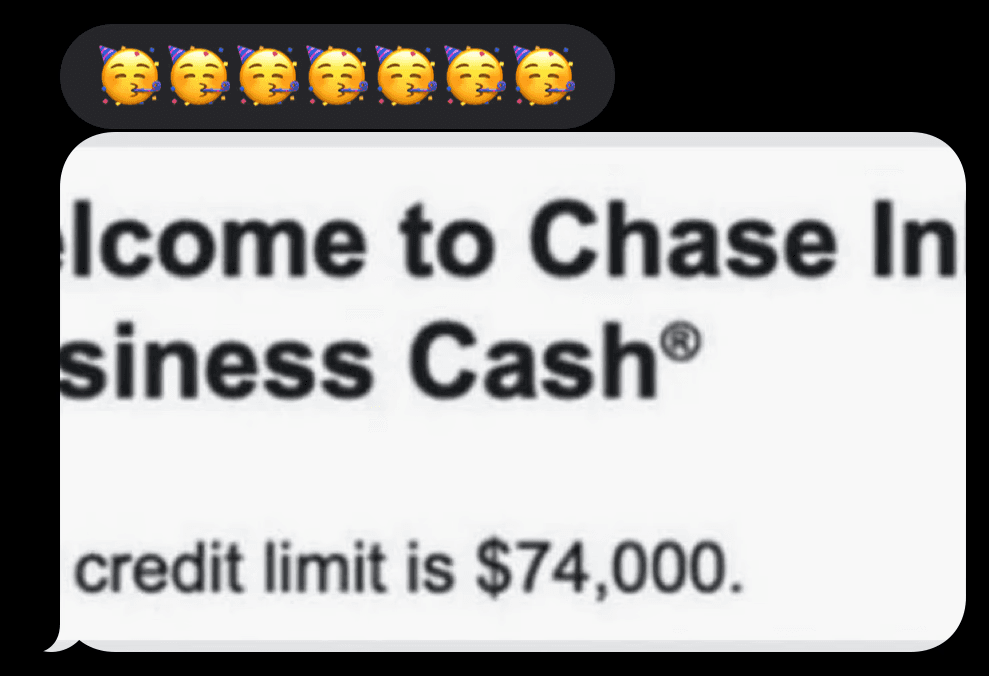

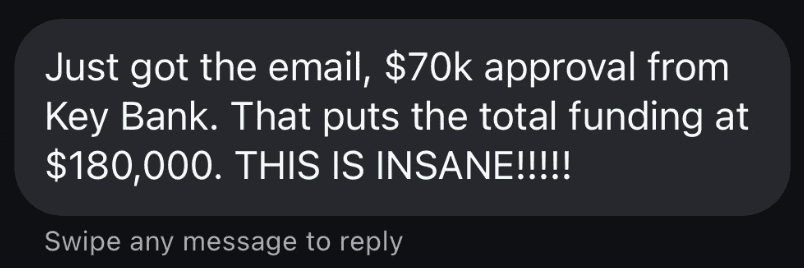

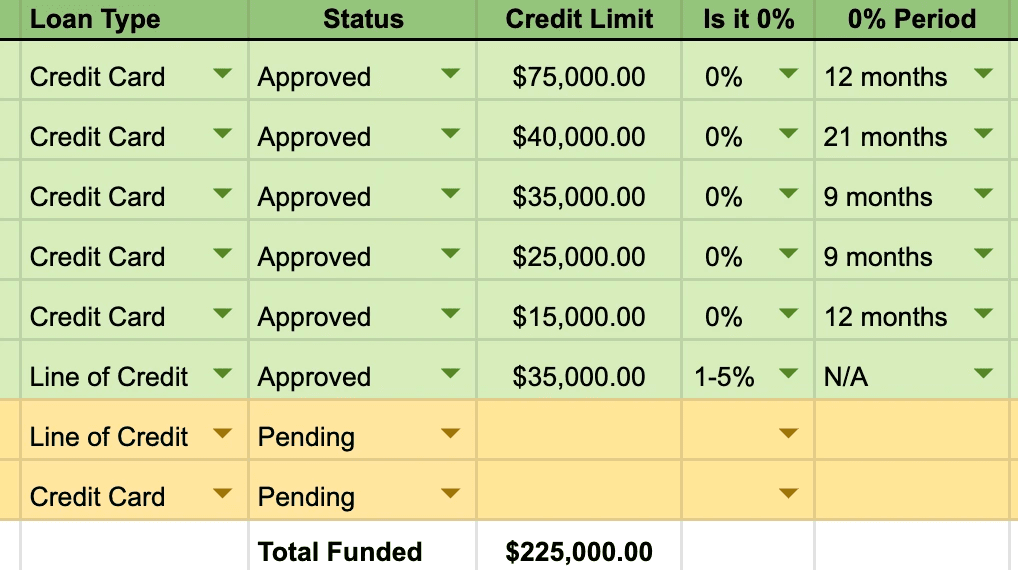

FROM 12 REJECTIONS

TO

$225,000 IN FUNDING:

Stop us if this sounds familiar:

You've been trying to get approved for funding so you can finally start growing your business the smart way…

You do all the research, read every article, watch more YouTube videos than you care to admit

Maybe you even start working with a funding company..

You have a list of banks you think you have a fair shot with.

You check the requirements, you fit those.

After all, your credit is pretty good.

Not perfect, but good enough.

You have every document you need.

Your business fits the bill. After all, you don't need millions. You just need enough to finally start buying back some of your time…

So you fill out the online application, double, triple, quadruple check all of your information..

Looks good.

You've crossed the t's, dotted the i's.

You hit apply.

A few hours later you get an email from the bank.

This is it, you're about to turn everything around.

"We regret to inform you that we can't

approve your business for a loan."

…

What happened?

Where did you go wrong?

It's not your fault.

You've been lied to

about what it takes to actually get approved for 0% interest funding.

See, banks have something called "internal scoring models".

These help banks decide whether to approve or deny credit applications.

Similar to how a college reviews a student's report card before admitting them into their school.

Or how a hiring manager has to review a person's resume before giving them the job position…

Banks have algorithms that look at your credit history, and in less than a second decides if you're worthy to be approved for funding.

These scoring models can have dozens of approval signals inside them.

And each bank has different approval signals that they update all the time.

So you have dozens of banks…

With dozens of signals per bank.

And this is a big problem…

Because if you don't match these approval signals damn near perfectly…

You won't get approved.

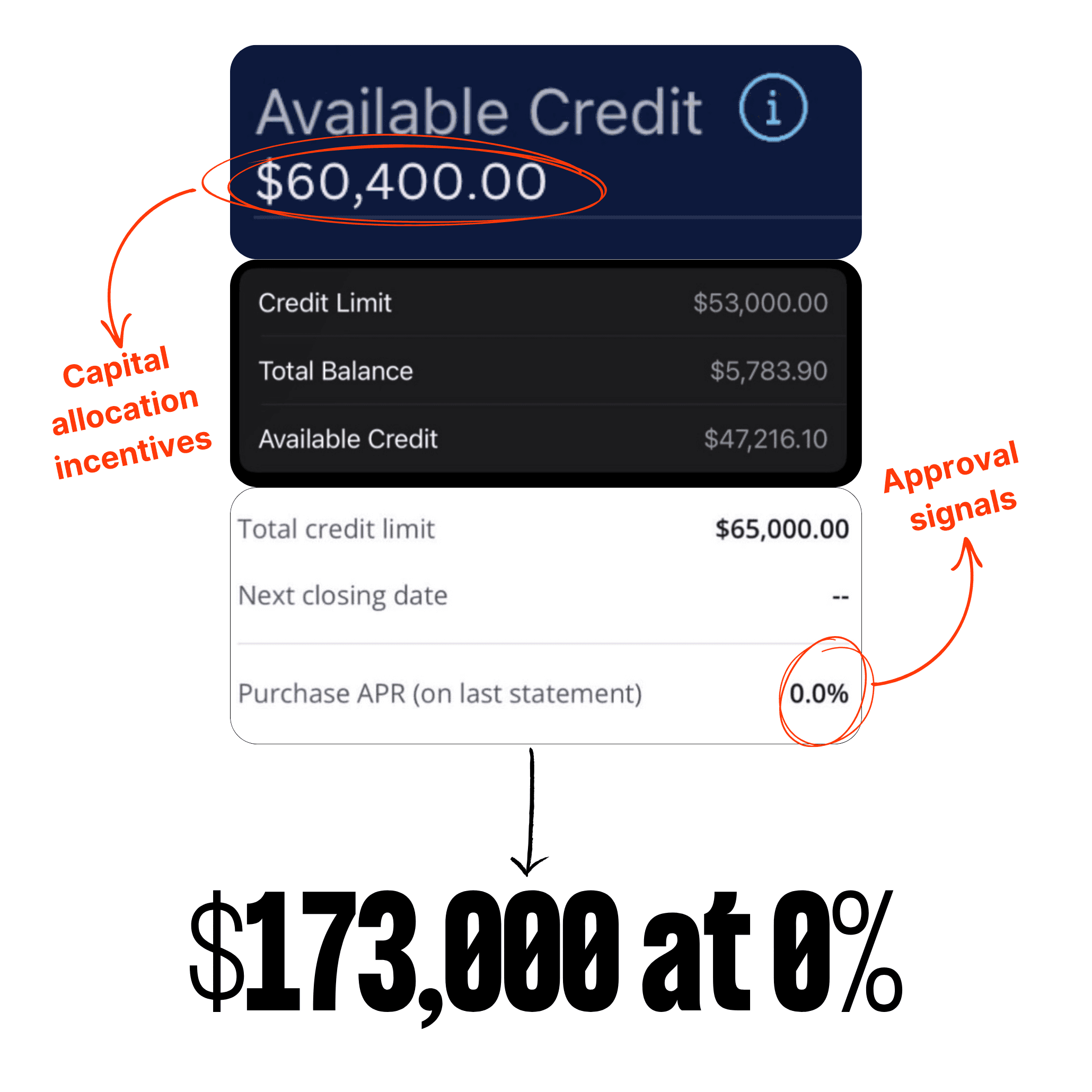

SO… HOW WELL DOES

FUNDING OPTIMIZATION

ACTUALLY WORK?

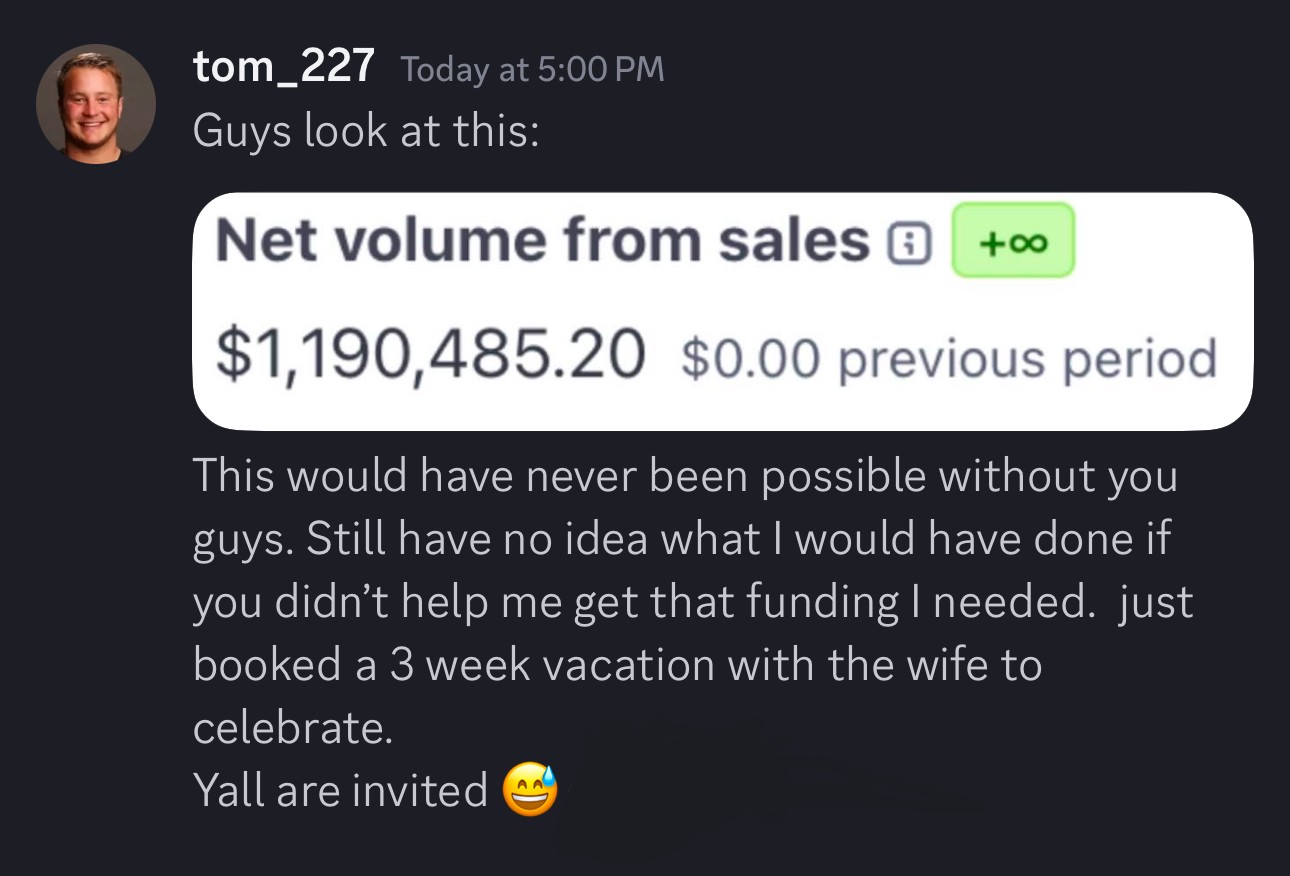

In just the past year we've been able to help our clients get approved

for a total of…

MILLION

sandra goes from borderline

bankrupt to getting approved for $90,000 in 0% interest capital

Sandra Miller

Founder of Titans Media

"It's like a 100 pound weight has been lifted off of my shoulders. I now have the breathing room to actually focus on growing my business, not just surviving the next months. Save yourself from the guesswork and just go straight to Citidel Consulting. I cannot tell you enough how much of a help they were. They don’t just fund your business. They set you up for life."

lars flips 2 extra properties,

netting him over $70,000 in pure profit after just 45 days of working with us

Lars Marston

CEO of Synergy Real Estate

"Citidel really isn't not like other funding companies. They really go out of their way to set you up for success. Because of them I qualified for $200k in funding and have flipped two extra properties this year all because I had the extra money to do it."

It works so well..

That we're giving the next

20 business owners a

"we definitely lost our minds" offer:

Here's exactly

what that looks like…

01. Free Blueprint Call

You'll be connected with a dedicated funding specialist who will analyze how many "red flag" items you have on your profile and create a custom optimization game plan.

02. Optimizing your profile

Within 24 hours our team of 15 funding optimization experts will prioritizing removing the worst offenders on your report using the bulletproof method we've developed over the past 4 years.

03. Tweaking your business

At the same time, we'll pick apart your business filling documents and position your business in a way that makes the banks see you as "safe bet" to give capital to.

04. 24/7 Updates

We'll keep you updated throughout every step of the way. And if you have any questions or concerns we'll be one text, email or phone call away.

Claim your free approval blueprint 👇